Black Scholes Pricing Model

What is the Black Scholes Model?

The 'Black Scholes Model' is one of the most important concepts in modern finance both in terms of approach as well as applicability and is widely used by option market participants. Fischer Black and Myron Scholes together developed a formula to compute the prices of European calls and puts based on certain assumptions in order to eliminate the risk factor.

This is a straightforward model which explains that the asset price follows a geometric Brownian motion that looks like a smile or smirk with constant drift and volatility.

The Black-Scholes model states that by constantly adjusting the proportions of stocks and options in a portfolio, the riskless hedge portfolio can be created by investors where all market risks are eliminated.

What are the Inputs required in Black Scholes model?

The inputs in the Black Scholes model are affected by five basic factors. The inputs in this model are spot price, exercise price, time to expiration, stock volatility, and interest rate. Let's understand these inputs in a little more detail-

Spot Price: It is simply the market price of the underlying asset on valuation date. In case of illiquid assets, it may be a difficult input to find but under normal scenarios the closing market price can be used.

Strike Price: It is the price level at which the option holder has the right to buy or sell the underlying asset. This input will always be given in the option contract so you don’t need to worry about this.

Time to Maturity: It is the time period (in years) until which the contract expires.

Risk free Interest Rate: The yield on zero coupon government bond is usually taken as risk free interest rate.

Volatility: It is probably one of the most important input in option pricing model. You can calculate volatility in different ways.

Historical volatility can be calculated using historic price data for the movement of share price. Usually you should calculate data over a longer time frame say more than five years. However, there are many flaws in historical volatility as it assumes that the past will reflect the future which is not the case always.

Hence you should use forward looking measures like implied volatility to avoid this shortcoming and to make calculation more realistic.

Let’s understand the concept of implied volatility:

Implied Volatility is a volatility implied by the market price of trading options. Since the volatility is unknown (which is an input here) and the price is known, the pricing model is reversed to determine the volatility. You need to be aware of the volatility surface when using implied volatility. Volatility surface is three-dimensional representation of the relationship between volatility, option life and exercise price. So, in order to use implied volatility, the option from which the volatility is implied should have a relationship between volatility, option life and exercise price.

Assumptions of Black Scholes Model

Through this model, one can compute the value of stock options and can be used to compute the values of both call and put options. This model is based on a number of assumptions which are to be carefully studied in order to have a better grasp over the topic.

(i) Constant volatility: Volatility is a measure of how much a stock can move in the near term. It is assumed to be constant over time. This implies that the variance of the return is constant over the life of the option. However, in real life trading this condition doesn’t apply.

Volatility can never be constant in the longer term rather can be relatively constant in a very short-term horizon. This is the reason why some advanced option valuation model substitute with stochastic process generated estimates over Black-Scholes’ constant volatility.

(ii) No dividends: Next assumption is that the underlying stock does not pay any dividend during the life of the option which practically seems very unrealistic as most companies pay dividends to their shareholders.

A simple way of adjusting the Black Scholes models for dividends is to simply deduct the discounted value of a future dividend from the stock price.

(iii) Efficient markets: Another important assumption of Black Scholes model is that they assume markets to be fully efficient where all participants have equal access to available information and at the same time, the markets are assumed to be liquid. This assumption of an efficient market suggests that people cannot predict the price movement in a consistent manner. The Black-Scholes model assumes that stocks move in a manner referred to as a random walk. Random walk means that at any given moment in time, the price of the underlying stock can go up or down with the same probability. This is not the case in the real world as the market may remain inefficient for a prolonged period of time.

(iv) Log-normally distributed returns: Next assumption is that returns on the underlying stock are normally distributed. This assumption is very reasonable in the real world.

(v) Interest rates are constant and known: The Black Scholes model also assumes interest rate to be constant. Hence the model uses risk free rate to represent constant and known rate. So, the market participants can both borrow and lend at this rate but in the real world, risk free rate doesn’t exist.

(vi) No transaction costs and commissions: This assumption states that there are no barriers to trading i.e. there are no transaction costs or any commission associated with the buying or selling of assets.

(vii) European-style options: The Black-Scholes model assumes European-style options which can be exercised only at expiration date. It does not take in consideration American-style options that can be exercised at or before expiration of the contract, making it more valuable due to higher flexibility.

(viii) Liquidity: This model assumes that markets are perfectly liquid and you can purchase or sell any volume of stock or options at any point of time.

Black Scholes interpretation:

Keeping in mind the above assumptions, suppose there is a derivative security which is trading in the market. This security will have certain payoff at a future specified date, depending upon the stock price to that date. It is little surprising that the price of a derivative is determined at the current moment while the stock price follows a random walk which cannot be determined at the current time but in the future.

However, in case of European call or put option, Black Scholes stated that it is possible to create a hedged position where you will have a long position in the stock and simultaneously a short position in the option whose value will be independent of the stock price”. This dynamic hedging strategy resulted in a partial differential equation which guided the price of option which can be understood through the Black Scholes formula.

Black Scholes equation

The Black Scholes equation is a partial differential equation, which explains the price of an option over time. The equation is shown below-

The idea behind the equation is that you can easily hedge the option by buying and selling the underlying asset in just the right way and thus eliminating the risk factor. As per this hedge, there is only the right price for the option which is explained by the Black Scholes formula.

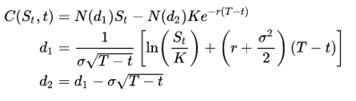

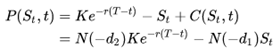

Black Scholes formula

The price of a European call and put option can be computed using the Black Scholes formula. This price is consistent with the above discussed Black Scholes equation as the formula can be obtained by solving the equation for the corresponding terminal and boundary conditions.

In terms of the Black–Scholes parameters, the value of a call option for a non-dividend-paying stock is:

Based on put–call parity, the price of corresponding put option is-

Where,

- T-t is the time to maturity (in years)

- N is the cumulative distribution function of the standard normal distribution

- St is the spot price of the underlying asset

- r is the annual risk free rate (expressed in terms of continuous compounding)

- σ- is the volatility of returns of the underlying asset

- K is the strike price

Black Scholes Option Pricing model played a very important role at articulating pricing of options and corporate bonds on the assumption that a risk-free interest rate existed. Even today it is used for estimating the worth of options but it is applied mostly in academics and in portfolio management departments of big institutions.

There are a number of reasons for wide use of this model in spite of several loopholes. The most important one is that it provides a framework for options pricing and gives a good approximation to the pricing of options. Another important reason for studying the Black-Scholes theory is that it is used as a standard in the financial world. In many cases, traders quote the Black Scholes volatility to each other than actual prices of the option.