How Do Credit Cards Work?

Understanding how credit cards work will help us understand the various aspects of credit cards.

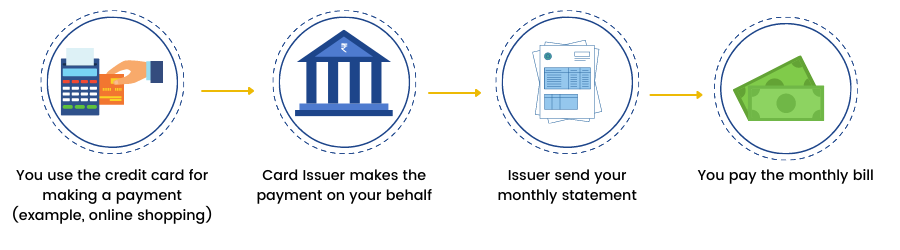

Simply speaking, when you use a credit card for a transaction (say online shopping), you do not pay anything at that point in time. Instead, the card issuing bank or non-banking financial institution (NBFC) pays on your behalf. You can use the credit card as much as you want till you exhaust your approved limit.

At the end of 30 days (every card has a credit cycle….more about this later in this section),the bank or NBFC will send you a credit card bill. This is the time when you have to make the payment. You have the option of paying this bill in full or make a part payment. In case you pay it in full, you don’t have to pay any charges. However, if you make a part payment, interest will be levied on the remaining amount and added to your next monthly bill.

Let’s see a quick snapshot of what we just discussed:

Credit card statement

Let’s first see how a credit card statement looks and then understand its components one by one:

1. Statement date: The date on which the statement has been issued. This remains the same every month. For example, in the given example, the statement has been issued on October 28, 2020. This means that for this credit card, the statement is issued on the 28th of each month.

This brings us to the concept of billing cycle which is the 30 day period for which your credit card statement is issued. For the above example, the billing cycle of the card in the above example is from the 29th of month 1 to the 28th of month 2.

2. Payment due date: This is the date by which the credit card payment has to be made. In the case at least the minimum balance amount due is not paid by the due date, a late payment charge is levied (discussed in the next section). For example, in the above example, in case the minimum payment amount of ₹ 200 is not paid by November 15, 2020, a late payment charge will be levied.

3. Total amount due: This is the total amount that you need to pay back to the bank/NBFC for the usage of the credit card in the previous 30 days. If you pay this amount in full, you will not be charged any interest. Any part payment will attract interest charges on the remaining amount.

4. Minimum amount due: This is the minimum amount that you have to pay to the bank/NBFC. Usually, this is 5% of the total amount due. Non-payment of minimum amount will not only attract late payment charges but may also lead to severe actions from the lender’s side such as card blockage, calls from the bank/NBFC or more severe actions as deemed fit by the issuing authority.

5. Previous balance: This is the total billed amount in the previous statement (i.e. bill generated on September 28, 2020.

6. Purchases/charges: These are all the transactions done during the billing month, where you have used the credit limit.

7. Cash advances: In case you have withdrawn any cash from your credit card, it will appear here.

8. Payment/credits: This section contains details of all payments you have made during the billing cycle. Hence, your previous payment will reflect in this segment. Also, in case you have received any other credits such as cashback or refund of any payment, that will also show here.

9. Credit limit: Every credit card has a credit limit, which is the maximum amount of money you can use. As mentioned earlier, this is determined based on a person’s credit history and repayment capacity.

10. Available credit: This is the unused amount of credit in the card. For example, if your total credit limit is ₹ 100,000 and you have used ₹ 40,000, then the available credit limit in your card is ₹ 60,000.

11. Cash limit: Some credit cards may allow withdrawing cash from the credit card. This limit is known as the cash limit. However, remember, this advance entails very high-interest charges and hence should only be used in the times of utter necessity.

12. Available cash: Similar to the available credit card limit, this is the unused amount of cash limit in your credit card.

Other common terms related to credit cards:

Now, let us discuss some terms you will commonly hear with regards to credit cards:

Balance transfer: Sometimes, people transfer the outstanding balance from card A to card B. This process is known as a balance transfer. The primary reason for doing this is that card B may have a lesser interest rate than card A or may offer an EMI option to pay off the bill faster. Of course, other benefits may also be there. However, please note that either card A or card B may charge a fee for such balance transfer (commonly known as balance transfer fee). Hence, find out about it before you make a balance transfer.

EMI: While making transactions of a certain amount and above, you will be given the option to pay in full or convert the payment into monthly EMIs. You can choose to convert the entire payment into EMIs for 9-month, 6-month, 9-month and so on. Sometimes, banks offer conversion into EMIs with no interest. However, you may still be charged a processing fee. This is a convenient method to finance your expenses.

Every lender has its own process of converting to EMIs. Usually this can be done online through the lender website. You may also call customer care and opt for EMIs.

OTP: OTP or one-time password is a code that is SMSed/emailed to you while using your credit card online. This is a security code which is sent to your registered mobile number or email id or both. Ensure that you do not share this with anyone else. This code also ensures that your credit card is not being used by any unauthorized person. Until and unless you input the OTP, an online transaction will not be successful.

Ready to master finance from A to Z? Enroll now and unlock the secrets of credit cards and more!