Analyse Inter-relationship between Stocks and Other Asset Classes

By now you have understood how equities move and from earlier sections you have a basic understanding of how various asset classes react to each other.

Let's now move to learn how other asset classes like Bonds, Commodities and Currencies impact Equity returns.

Stocks vs Bonds

Bonds and stocks are positively correlated since both stocks and bonds are inversely related to interest rates.

Rising bond prices (due to falling interest rates), make it cheaper for the corporates to borrow. This helps them to improve their bottom line and hence the corporate profits.

Our earlier discussions showed how growth in corporate profit has a positive impact on the stock price returns. Therefore, rising bond prices are a direct indicator for stock prices to rise.

Similarly, a falling bond price (due to rising interest rate) would make it costlier for companies to borrow hence dampening the bottom line. This would lead to lower stock prices. Therefore, you should expect a fall in stock prices in case the bond prices have started to fall.

Case Study - IL&FS Crisis

Somewhere around September 2018, the dark clouds of defaults had started to take the shape. The first burst among the series of defaults was IL&FS. This led to a series of defaults by Dewan Housing, Yes Bank, IndiaBulls Housing and many more.

Interest rates reflect the risk premium over the risk free rate. This premium is referred to as credit spread and is calculated as the difference between a corporate bond yield and a government bond yield of the same maturity. In case of such big defaults it was quite obvious that the risk would increase and consequently hike the credit spreads.

As shown in the above graph, the credit spreads were in a narrow range of 50-100 bps during April-September 2018. Post the unfolding of the IL&FS crisis , the credit spreads shot up to more than 150 bps.

A similar trend was seen when the government announced the first lock-down somewhere during March-20.

Lets see if we could have benefitted by this data in our equity trades.

From the period of September 2018 till October 2018, The SENSEX corrected by approximately 15%.

The rise in the bond yields led to falling bond prices. Since equities are positively correlated to bond prices, a similar trend was seen in them.

Stocks vs Commodities

A rise in commodities has a direct impact on inflation and it starts to rise.

Remember, equities are directly proportional to inflation. However, not hyperinflation. In the previous segments we discussed that only the inflation that is within the target range of RBI is healthy and beneficial for stocks.

Or, if commodity price increase is sustainable with the growing income, it will generally lead to higher equity prices.

What if commodity prices rise more than the income increase, which is mostly the case in a commodity bull cycle. In such cases, inflation is probably dominating the interest rate increase (hyperinflation) rather than GDP growth. This is particularly seen in Phase III. In such cases, equity markets react negatively and fall.

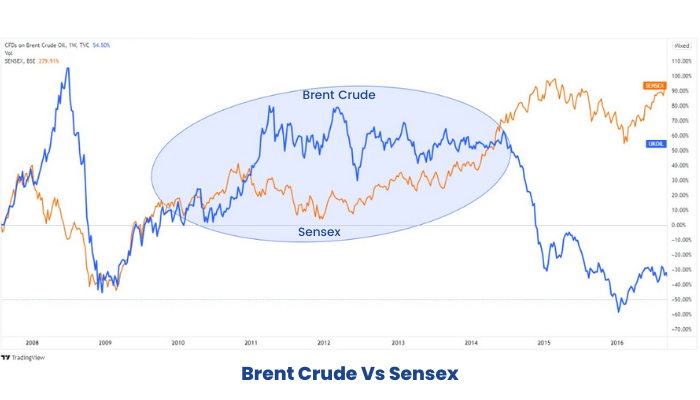

Case Study: Crude at All Time High (2012-2013)

Brent crude rose to an all time high of USD130 per Barrel led by European debt crisis and Civil War in Libya during 2011-13. See in the below chart, how an above average inflation in crude oil prices led to SENSEX shredding in valuation.

In the chart, you can also notice how SENSEX kept on rising once the supply of Crude oil increased and prices suppressed post 2014.

Therefore, an abnormal increase in commodity prices leads to fall in equities as that indicates falling purchasing power (inflation).

Stocks vs Currency

Currency has a direct bearing on commodity prices.

For a commodity importer country, devaluation of currency means higher commodity prices. This makes the environment conducive for runaway inflation (read, inflation exceeds RBI’s target range) and the ultimate diminishing of stock valuations.

Conversely, a rise in the currency of a country would mean lower import prices. Such instances would cool down the inflation (read, inflation is in RBI’s target range) and hence lead to a rise in equity prices.

However, a clear cut relationship between stocks and currency prices is difficult to state. In the above example, say the commodity importer country, would also be a service exporter, like India. In that case if India’s currency becomes too strong against counterparty countries, this would make its services costlier and hence India might lose its cost competitive advantage against other countries. In such cases, the fall in GDP might outweigh the inflationary advantage with falling commodity prices and consequently stock prices might fall.

Lastly, remember, intermarket analysis is not a method that will give you specific buy or sell signals. However, it does provide an excellent confirmation tool for trends and will warn of potential reversals.