General Portfolio Policy: The Defensive Investor

The general perception is that an investor should earn a return according to the level of risk they take. But for the author, an investor should be earning returns on the amount of intelligent effort they are willing and are able to bear for this task.

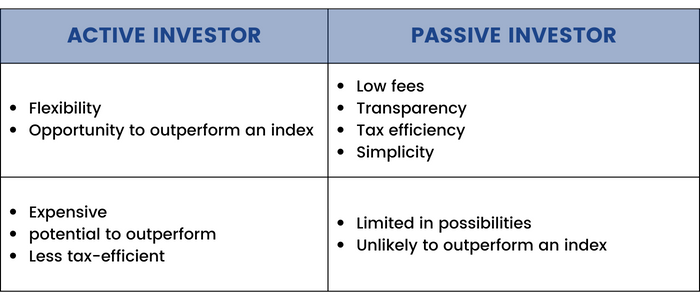

There are two types of investors:

Active investor: One who continuously keeps buying and selling at regular intervals. An enterprising investor is the one who uses maximum intelligence and skill for this purpose. Graham says an enterprising investor is someone who can devote a fair amount of his attention and efforts towards achieving better than average returns.

Passive/defensive investor: One who buys and holds a stock for a long period. The minimum return will go to passive investors, because they tend to use a simple buy and hold strategy.

In some cases, an investor might end up buying cheap which can offer a chance of making larger profits.

In general, people are better suited as a defensive investor because the time and dedication needed are very limited from their side.

Passive investment also requires fewer taxes, less commission, and a possibility of better returns. The author mainly talks about 2 investment products, i.e., stocks and bonds (mainly high-grade bonds).

The investor should allocate 50% of his value in stocks and 50% of it in bonds. A defensive investor should be satisfied with average returns because of the little research, time, and effort they are willing to give while doing their due diligence. Also, portfolio rebalancing is required when the stock falls out of the 50-50 target.

For example- if the stock rises 10%, then the total weight of stock becomes 55%, the investor should sell 5% of his stock value or buy more bonds to make it equal again. Also, if the investor has less expertise in stocks, they might allocate 75% in bonds and gradually decrease stocks to 25%.

Yale University had followed a similar method after 1937, but it had around 35% allocated to common stocks and in around 1961, 61% was allocated in equities. Market advancement was the reason for this rise of 26% and that is why the author suggests that we should frequently keep rebalancing our portfolio.

The Bond component:

There are two factors concerning bonds:

1) Taxable or tax-free bond- The tax decision should be a question, whether an investor’s income is actually above or below the tax bracket.

For example, consider 2 investments:

a) A 7.5%, 20 year “Aa” rated corporate bond.

b) A 5.5% tax-free bond.

For a general investor, the first option seems better. But consider an investor who is in a maximum tax bracket of 30%. If he selects option "a", his after-tax returns would be 5.3%. Whereas if he would have selected option "b" he would have generated a higher return of 5.5%. So, we should always consider post-tax returns when investing in bonds.

Tax Rate = 30%

2) Maturity- The author advises investors to sacrifice a small % of yield to purchase a non-callable bond of 20-25 years. Graham also states that there is an advantage in buying a low coupon bond at a discount than a high coupon bond at par.