Depreciation

Secondly, let us start with depreciation which is the loss in value of an asset over the period of its useful life.

What is Depreciation?

- Depreciation is a method of allocating the cost of a tangible asset over its useful life of several years.

- Depreciation is a non-cash item.

In simple words we can say that depreciation is the reduction in the value of an asset due to usage, passage of time, wear and tear, technological outdating or obsolescence, depletion, inadequacy, rot, rust, decay or other such factors.

Why Depreciate?

Depreciation helps in smoothing the income statement by allocating the cost.

Suppose a ₹500 asset is bought in FY 2010 which is going to be used for the next 5 years. It won’t be right to have ₹500 as expense in FY 2010; instead, the ₹500 should be spread over five accounting years (the useful life).

Depreciation is also used for tax purposes – as a way to lower tax expenses. Since it is a non-cash item, it does not reduce the cash balance of a firm, however, it helps in savings of the tax expense since the recording of depreciation will cause an expense to be recognized, thereby lowering stated profits on the income statement.

Depreciation Schedule

COMMONLY USED DEPRECIATION TECHNIQUES

Straight Line Depreciation

a)Simplest and most commonly used method.

b)Calculated by taking the purchase or acquisition price of an asset, subtracting the salvage value and then dividing by total useful years.

Depreciation = (Cost of an Asset- Salvage Value)/Useful life

Where,

- Cost of the asset is purchase price or historical cost

- Salvage value is value of the asset remaining after its useful life

- Useful life of the asset is the number of years for which an asset is expected to be used by the business

c)Depreciation is also used for tax purposes – as a way to lower tax expenses.

d)Produces a constant depreciation expense.

Example: - Consider an asset that costs ₹35,000 with an estimated useful life of 7 years and has a salvage value of ₹5,250. Under the straight-line method, the depreciation expense per year will be –

Depreciation expense = (35,000-5,250) /7 = ₹4,250 per year

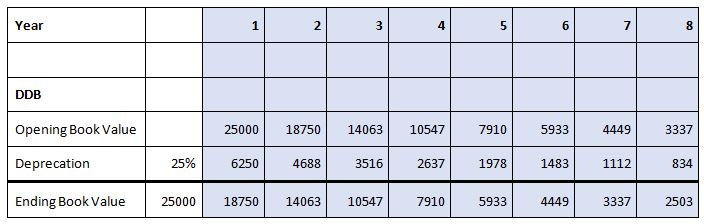

Accelerated Depreciation

a)Allows companies to write off their assets faster in earlier years than the straight-line depreciation method and to write off a smaller amount in the later years.

b)It recognizes higher depreciation expenses during the earlier years as compared to the straight-line method of depreciation.

c)The major benefit is to provide a tax shield. In the initial years, the depreciation is higher as a result of which, tax charged on the profit is less compared to the later years. This results in deferment of tax liability since income in earlier years is lower.

d) There are two popular methods – Double Declining Method and Sum of Years’ Digits Method.

Double Declining Method – In this method, a fixed rate of depreciation is charged on the net value of the fixed asset at the beginning of the year. The rate of depreciation charged under this method is twice the rate that is charged under the straight-line method. The method reflects that assets are more productive in the earlier years as compared to their later years.

Depreciation Expense = 2 x Straight-line depreciation rate x Book value at the beginning of the year.

Example: - Consider a piece of property, plant, and equipment (PP&E) that costs ₹25,000, with an estimated useful life of 8 years and a ₹2,500 salvage value. To calculate the double-declining balance depreciation, set up a schedule:

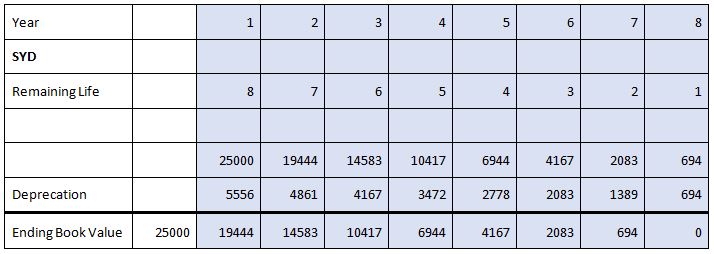

Sum of the Years’ Digits Method – In this method, the remaining useful life of the asset in a particular period is divided by the sum of the years’ digits. This fraction is then multiplied by Depreciable Cost. It recognizes depreciation at an accelerated rate.

Depreciation Expense = Depreciable Cost * (Remaining useful life of an asset/Sum of Years’ Digits)

Where,

Depreciable Cost = Cost of asset – Salvage Value

Sum of Years’ Digit = n*(n+)/2, where n = useful life of asset

Example: - Consider a piece of equipment that costs ₹25,000 and has an estimated useful life of 8 years and a ₹0 salvage value. To calculate the sum-of-the-years-digits depreciation, set up a schedule:

Depreciation & Cash-Flow Statement

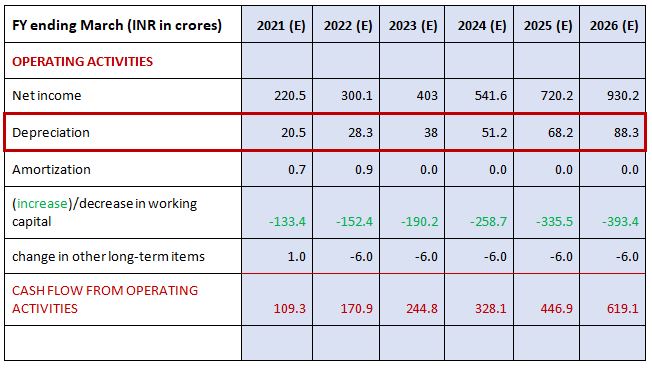

Depreciation is a non-cash expense.

Indirect cash-flow statements start with net income.

Net income includes depreciation expense.

Hence depreciation expenses are added back to Net Income to calculate the Operating Cash Flow.

Adding Back Depreciation

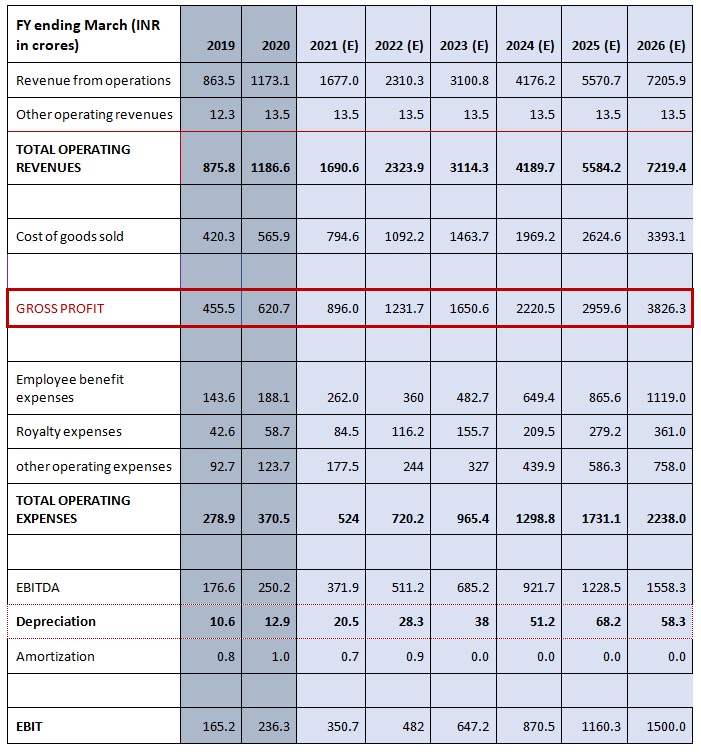

Depreciation & Income Statement

Depreciation expense is linked to the income statement below the EBITDA (Earnings before Interest, Taxes, Depreciation and Amortization) to calculate EBIT (Earnings before interest and taxes).

Linking Depreciation to P&L

Depreciation & Balance Sheet

The ending property, plant, and equipment (PP&E) calculated in the depreciation schedule should be linked to the Balance Sheet.

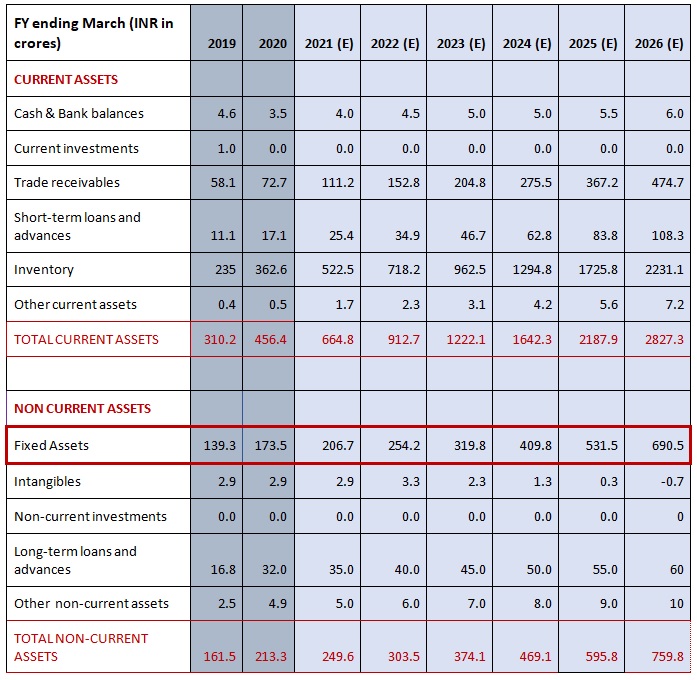

Linking PP&E to Balance Sheet

The Fixed Assets in the Balance Sheet will be net of the depreciation for that year.