Post Office Recurring Deposit

Earlier, we have discussed Recurring Deposits offered by Banks. In the section, we will focus on Recurring Deposits offered by the Post office. However, the concept remains the same; there are a few key differences between them. So, let us begin.

What is a Post Office Recurring Deposit?

It is an account wherein an individual can deposit any amount (minimum of ₹10) in multiples of ₹5 each month for a minimum period of 60 months and earn a fixed interest on the deposits. The account can be opened in any Post Office across India. A recurring deposit has a lock-in period, but it can be pre-matured only after 1 year after paying a penalty. One can also borrow from the recurring deposit.

How to Open a Post Office Recurring Deposit Account?

The following documents are required to open a Fixed Deposit account:

- Fill the Post Office Recurring Deposit (RD) Account Opening Form.

- Furnish all details provided in the form like PAN details, address proof, nomination details.

- One must carry the original PAN Card, Address Proof, and ID proof for the in-person KYC verification purpose.

- Submit the same and start operating the account.

It is not necessary to have a savings account in the same post office where the RD account has been opened. But it is beneficial to start a Recurring Deposit in the post office where one holds a savings account to get the interest credited.

Interest Rate Mechanism

For Recurring Deposits, interest is compounded quarterly. Presently, the interest rate is 7.3% p.a. The interest rate is linked to G-Sec rates. The interest rate is subject to change as and when G-Sec rates change, but once a Recurring Deposit is booked, the interest rate prevailing at the time of booking the Recurring Deposit would hold till maturity.

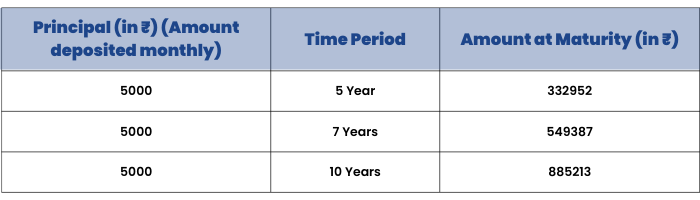

The following table shows what would be the amount receivable at maturity if we invest ₹5000 monthly for different time periods:

Tax Implications

There is no tax relief for Recurring Deposits. The interest earned is subject to taxation. TDS is not deducted from the interest earned. However, there is an exemption limit of up to ₹50000 on the interest earned for senior citizens.

Risk associated with Post Office Recurring Deposit

There is no risk involved as these deposits are backed by the Government of India. Principal and Interest are guaranteed. If inflation turns out to be higher than the nominal interest rate of the Recurring Deposit, there would be no real returns available. Hence, it is not inflation protected.